Meta Research Report - StockStory

Looking back on social networking stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including Meta (NASDAQ:META) and its peers. Businesses must meet their customers where they are, which over the past decade has come to mean on social networks.

Shares of social network operator Meta Platforms (NASDAQ:META) jumped 6.6% in the afternoon session after the major indices popped (Nasdaq +3.4%, S&P 500 +2.5%) in response to the positive outcome of U.S.-China trade negotiations, as both sides agreed to pause some tariffs for 90 days.

Volatility in the Market

Volatility cuts both ways - while it creates opportunities, it also increases risk, making sharp declines just as likely as big gains. This unpredictability can shake out even the most experienced investors.

At StockStory, our job is to help you avoid costly mistakes and stay on the right side of the market.

Meta Platforms Overview

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ:META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Reality Labs.

:max_bytes(150000):strip_icc()/META_2022-07-24_14-59-04-947e9b64b5de4ad48eb988e4c8492a78.png)

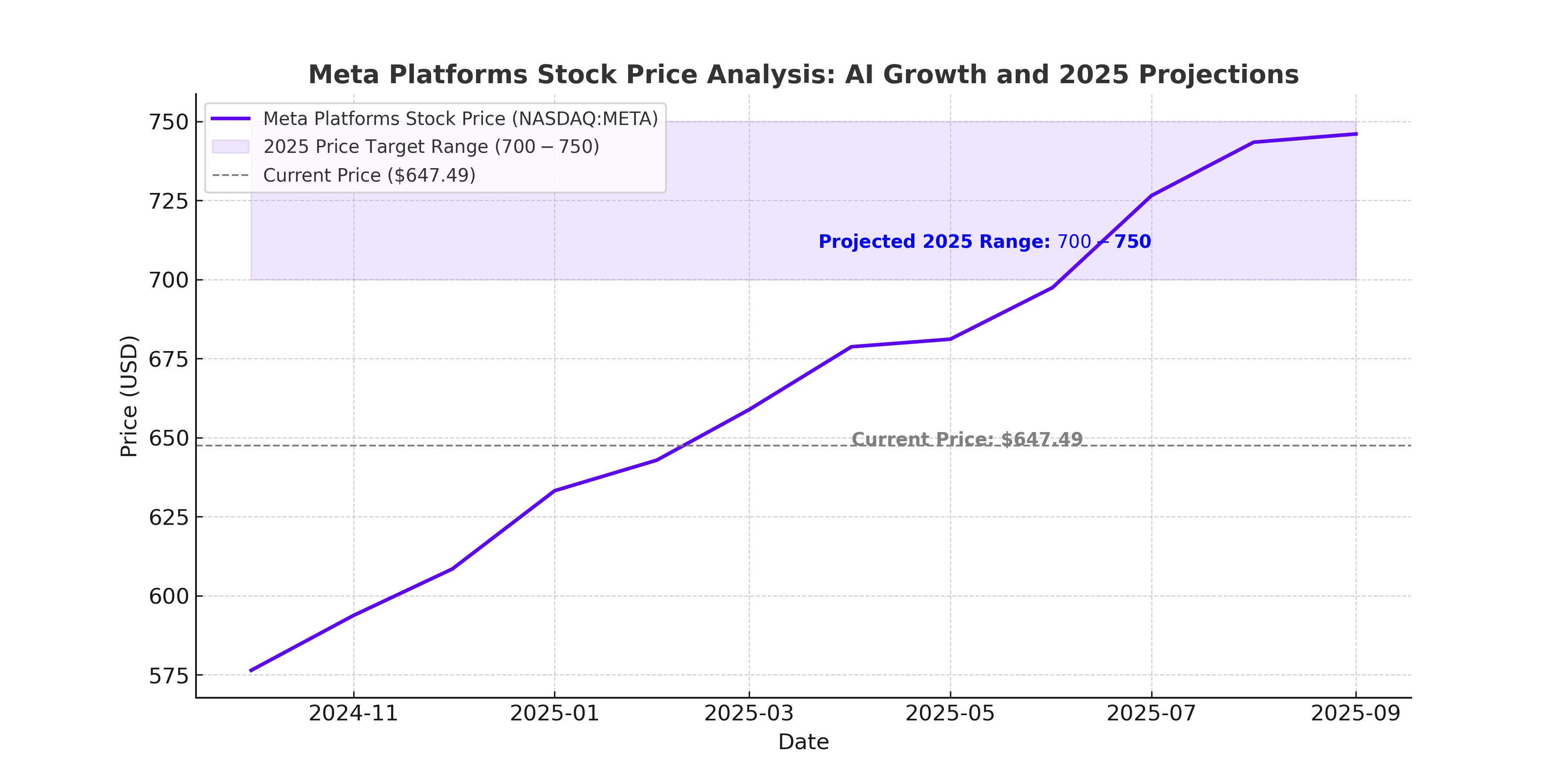

At $628.25 per share, Meta trades at 14.5x forward EV/EBITDA. Our work shows that buying high-quality companies and holding them routinely leads to market outperformance. If you can get an attractive entry price, that’s icing on the cake.

Financial Performance

Social network operator Meta Platforms (NASDAQ:META) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 16.1% year on year to $42.31 billion.

Meta Platforms competes with fellow social media advertising platforms like Google (NASDAQ:GOOGL), Snapchat (NYSE:SNAP), Twitter (NYSE:TWTR), and Pinterest (NASDAQ:PINS).

User Base and Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Meta’s sales grew at a decent 12.5% compounded annual growth rate over the last three years.

Meta's daily active people increased by 6.4% annually to 3.43 billion in the latest quarter. If Meta wants to reach the next level, it likely needs to innovate with new products.

Key Metrics

In Q1, Meta added 190 million daily active people, leading to 5.9% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

Meta’s average revenue per user (ARPU) growth has been exceptional over the last two years, averaging 13.3%. This quarter, Meta’s ARPU clocked in at $12.34, growing by 9.6% year on year.

Profitability and Efficiency

Meta Platforms boasts an elite gross profit margin of 82.1% this quarter, enabling the company to fund large investments in new products and marketing.

Meta is extremely efficient at acquiring new users, spending only 8.3% of its gross profit on sales and marketing expenses over the last year.

EBITDA and Earnings Growth

Meta has demonstrated elite profitability for a consumer internet business, with an average EBITDA margin of 60.3% over the last two years.

Meta’s EPS grew at a spectacular 24.7% compounded annual growth rate over the last three years, higher than its annualized revenue growth.

Conclusion

Over the next 12 months, Wall Street expects Meta’s full-year EPS of $25.64 to shrink by 3.7%. Meta has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products.